Merchant Routing Choice

Article contributor / Christine Lopez, SVP, SHAZAM Payments Network

When choosing where to route a transaction, merchants often consider the following:

- Ease of acceptance — Merchants want a frictionless experience for their customers, where they can quickly and efficiently make a purchase. This translates into transactions processed in less than one second.

- Network reliability — Merchants want to ensure a positive experience for their customers. Therefore, they want a network that offers high approval rates, along with 24/7, 365 availability.

- Network security — Security of a network is always top of mind for a merchant. They want to know the network they’re routing to is secure and has multiple, advanced layers of defense.

- Interchange rate — The interchange costs associated with a transaction is the major decision made by a merchant when deciding how to route a transaction. Merchants want to route to the lowest-cost network; however, not all merchants control their routing choice.

Large merchants may have the technology to route transactions where they deem to be the lowest-cost choice, or they may direct their processor to route transactions on their behalf. These merchants participate in routing agreements directly with the global networks that include reduced interchange rates at the expense of financial institutions.

Mid-size merchants usually participate in a service offered by their processor that will route based on the least cost to them.

The smaller merchants, those mom-and-pop stores on main street, usually don’t have a say in where their transactions are routed, as they can’t afford to participate in a processor’s routing service, or it’s not offered. Their processor will route their transactions to whichever network benefits them.

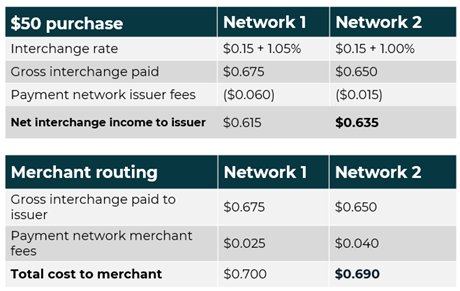

In the illustration below, the example shows when the network is a competitor, meaning they don’t take into consideration the impact to the financial institution when they’re negotiating interchange rates with a merchant.

As a financial institution, you would want the transaction to route on Network 2 as that network provides you with the greater net interchange.

.png)

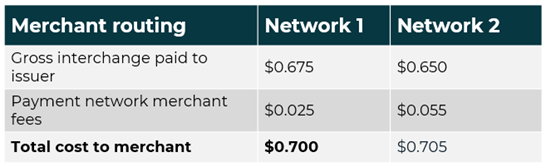

In the following illustration, the merchant would review the networks based on the gross interchange cost of the transaction and the network fees (or negotiated pricing) they would have to pay. In this example, Network 1 offers a lower merchant network fee which results in a half-cent saving for the merchant.

However, this causes a two-cent loss to the financial institution. This loss occurs for the financial institution because the network didn’t have their best interests in mind. They lowered their merchant network fees to win the transaction.

In many cases, global networks may provide merchants with special interchange rates that are significantly lower than the publicly disclosed rates or those communicated to financial institutions. It’s important to note that the networks' fees typically remain consistent with published prices.

SHAZAM® wants to ensure you receive the best net interchange on transactions. The illustration below shows how SHAZAM, as your partner, handles merchant special pricing. As you can see in this example, as Network 2, we also have the lower issuer fee.

Unlike the other networks that have higher issuer fees and then reduce the interchange a financial institution can receive, at SHAZAM, we consider all variables around rates and fees.

In this example, the merchant network fee was reduced so that the merchant would route to SHAZAM while providing our financial institutions with the best net interchange.

Sometimes SHAZAM is faced with the decision of how or if we should try to compete with the global networks to win transactions. SHAZAM does quite a bit of analysis to ensure we create a win-win situation for both merchants and financial institutions.

Financial institutions should consider the motivations of their networks. Does the network only look at lining their pockets? Do they want to win transactions at all costs? Do they take into consideration the financial impact to their bottom line?