Leverage Card Usage Data for Proactive Risk Management

Article contributor / Brooke Jacobson / Data Analyst

Financial institutions often feel as though their only position in the fight against fraud is reactive, but there are opportunities to use data from your debit card program to proactively manage risk.

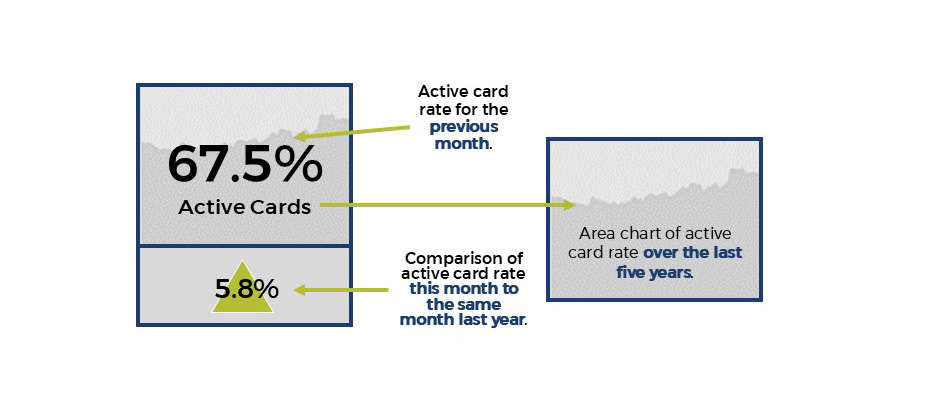

Calculating an active card rate comparing the number of cards used each month to the total number of active cards available for use helps identify a financial institution’s risk exposure. Debit cards that remain unused month after month represent risk. If these cards are lost or simply unmonitored, fraudulent activity can take place for longer before being identified, resulting in larger fraud losses. Monitoring and benchmarking your active card rate against historical performance and industry averages helps bring context and uncover if action is needed.

If your active card rate is declining or below an industry benchmark, conducting a card cleanup can reduce your risk exposure. Evaluating your procedures around issuance and monitoring activation rates can help you manage your active card rate moving forward.

Additionally, conducting a review of daily spending limits is another way to proactively manage your fraud risk. Review actual daily cardholder spending compared to daily limits to identify if there are opportunities to reduce daily limits without increasing inconvenience for your customers.

If a group of customers’ daily spending is consistently below your limits, you can reduce their spending limits and your fraud risk without a negative impact on those customers.

Contact your Client Executive to learn more about how SHAZAM® Business Intelligence Services™ can help you leverage your debit card data for decision making.