The true value of an association endorsement

Banking associations and credit union leagues across the country endorse financial service providers to provide their members with a trusted product and services solution. Their seal of approval provides additional credibility to the vendor by signaling that the association has evaluated and recommended them to their members. Here’s a general sense of how the process works and what it means for financial institutions.

Earning an endorsement

Having an association endorse a provider or prefer their services to their members varies depending on the association's vetting process and procedures. For Community Bankers of Michigan, where SHAZAM® has been a preferred provider for debit card, processing and ATM services for 15 years, it starts with a mutual interest between the service provider and their association to become a preferred provider, along with positive feedback from the association's members.

The provider then goes through a detailed due diligence process to ensure they are financially sound, have the necessary security safeguards in place to protect sensitive information and are compliant with federal and state regulations. “From our perspective the due diligence process is a comprehensive analysis of the business to not only ensure the business is in good standing but also to ensure that they are a true fit in the community banking industry,” says Kate Angles, Chief Operating Officer, Community Bankers of Michigan.

It’s a similar process to becoming a preferred provider for Independent Community Bankers Association of New Mexico, where SHAZAM is their preferred ATM and debit card processor. To be considered an ICBA/NM preferred provider, a company must be an established associate member with a proven record of serving their community banks. Applicants then submit detailed information about their financial stability, organizational structure and the value their services provide. That application is reviewed by their Products and Services Committee, followed by a presentation to the committee. The committee must then give a recommendation for approval before final approval is granted by the ICBA/NM Board of Directors.

“SHAZAM consistently supports our association’s mission through sponsorship, education and advocacy efforts that strengthen community banks across New Mexico,” says Chris Moya, President and CEO, ICBA/NM. “They provide reliable, innovative payment and fraud prevention solutions that help our member banks better serve their customers. Their alignment with our values and their genuine investment in our success makes them an indispensable partner to both ICBA/NM and our members.”

What it means for financial institutions

The focused engagement between a service provider and an association has benefits for financial institutions. The elevated status from earning an association endorsement ensures their financial institution members have access to innovative payment solutions, expert insights and the support of a strong strategic partner.

“Because of our due diligence process, we’re able to tell our banks that we’ve already done the laborious work,” says Angles. “We’ve given them that head start in their decision-making process when looking for a new vendor knowing that a CBM preferred provider has been vetted as an expectational option for them to partner with.”

Becoming a preferred provider is not a set-it –and-forget-it process. Both CBM and ICBA/NM annually review their partners to ensure these vendors continue to exceed the standards they met during the initial vetting process.

“ICBA/NM continues to prefer SHAZAM because they exemplify what it means to be a true partner to community banks,” says Moya. “They maintain a strong presence in New Mexico and across the country, providing reliable services while actively supporting our association’s mission.”

The power of partnership

SHAZAM makes it our business to advocate for community banks and credit unions. Like associations, SHAZAM ensures our members receive the highest value for the products and services we provide for them. This mindset is rooted in our membership structure. At SHAZAM, our members are our financial institutional clients who apply to become members. These members have a voice and a say in the direction of our company. And since SHAZAM serves members, and not shareholders, we are able to reinvest our profits into new technology to better serve our members.

“SHAZAM’s mission closely aligns with the mission and goals of CBM,” says Angles. “And in an industry where some salespeople over promise and the products and services under deliver, it's refreshing that SHAZAM does what they say in strengthening financial institutions.”

“The company’s member-owned structure, with community bankers serving on its board and advisory councils, reflects a deep alignment with the values and mission of community banking,” says Moya. “In addition, SHAZAM provides strong support to our association and actively contributes to promoting and advocating for the community banking industry. These qualities made SHAZAM an outstanding choice as an ICBA/NM preferred provider.”

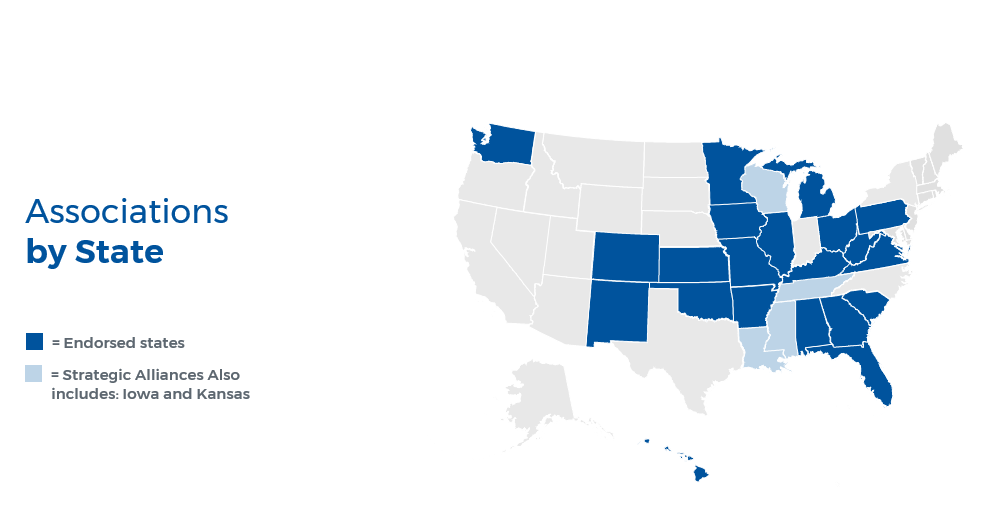

SHAZAM’s endorsements and strategic alliances

Many organizations recognize SHAZAM’s commitment to community financial institutions. SHAZAM recently became a strategic partner with the Iowa Credit Union League, one of three organizations with this honor. SHAZAM also earned additional endorsements from Community Bankers of Iowa and Community Bankers Association of Oklahoma. SHAZAM was also recognized with awards as a top vendor by Independent Bankers Association of Texas and Community Bankers Association of Illinois.

These endorsements and honors aren’t just handed out lightly. It’s the result of a constant commitment, and a shared vision, in service to state associations nationwide and their members. Visit our website to see a list of state associations that endorse our products and services to their members.